While interest rates on UK savings accounts have dropped to a miserable 1.1% and millions of Britons have been pushed toward financial uncertainty, one of the most enigmatic figures in the world of finance has decided to break his silence. Professor William Ashford, a world-renowned mathematician, turned down a colossal offer from Wall Street — to put his investment technology in the hands of ordinary British people. We met him at his office in London to understand why he decided to challenge the system.

The Man Who Said No to Wall Street

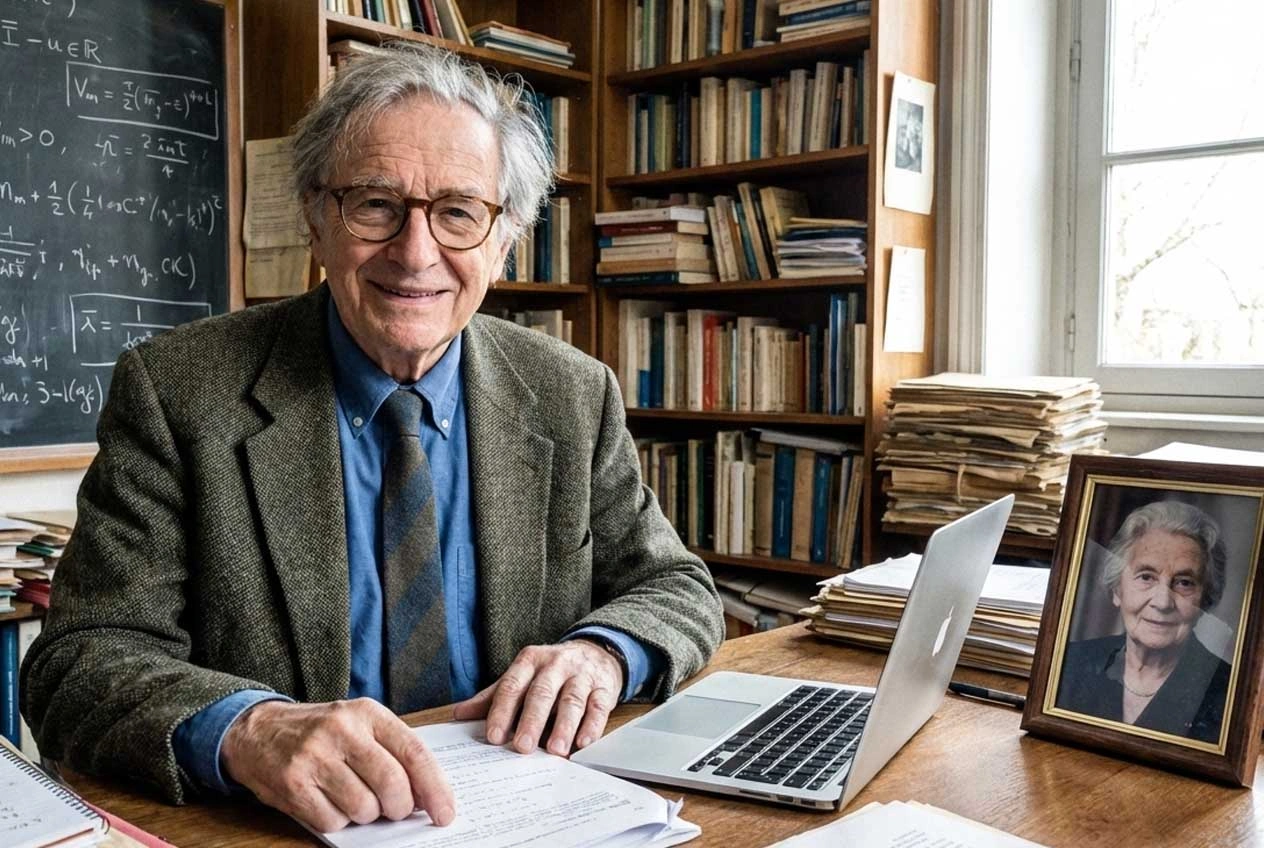

The apartment is on a quiet side street in London's Mayfair neighbourhood. No flashy luxury, no marble. Just stacks of scientific journals and the smell of old paper. Professor William Ashford, 71, welcomes me with a polite, slightly distracted smile. He is the man who two years ago in Geneva received the prestigious European Award for Research in Nonlinear Dynamics. That recognition caught the attention of the largest American investment funds. He was offered £60 million for his algorithm. He declined.

Michael Carter: Professor Ashford, let's start with the most surprising thing. £60 million. Very few people would refuse a sum like that, especially at 71. Why did you say no?

Prof. Ashford: (Smiles sadly and looks at an old photo on the desk.) You know, Michael, at my age you start counting what remains — not what you've accumulated. If I had accepted that money, the algorithm today would be locked in a digital safe. It would serve to make billionaires even richer — or worse, it would be useful to no one.

I spent 11 years developing this system. At first it was a purely academic project on nonlinear dynamic systems. But then it became personal. My wife, Catherine… (He pauses, his voice softening.) She fell ill a few years ago. We had savings, we had been careful our whole lives. But I saw how quickly financial security can vanish when the system works against you. I saw my colleagues — professors, tradespeople — people who had worked 40 years and were now worried about being able to heat their homes in winter, even with money in the bank. I realized that the mathematics of British savings had become the mathematics of losses.

Michael Carter: That's a harsh judgment. You speak of losses, yet savings accounts remain the preferred instrument for many Britons.

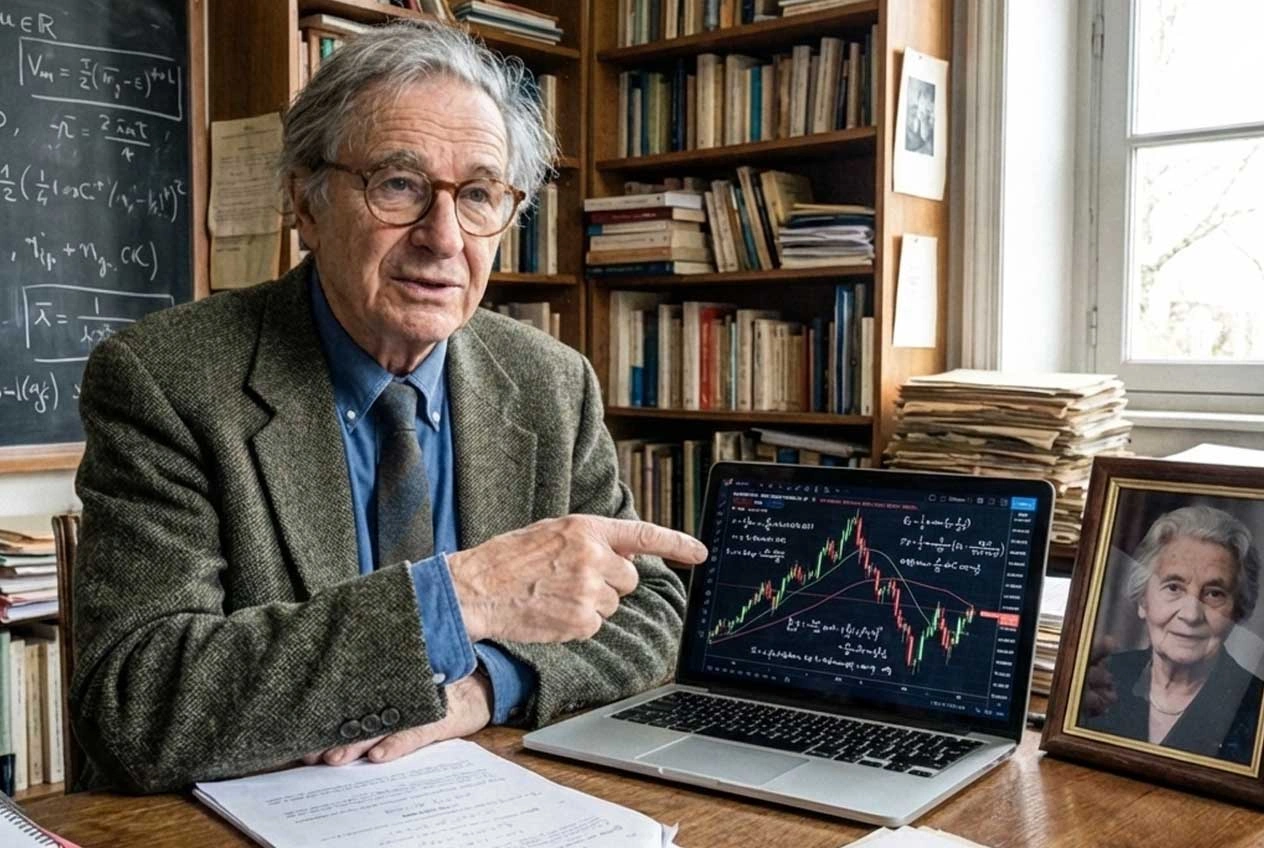

Prof. Ashford: (Calm, but firm.) It's an illusion, Michael. Look at the February 2026 data. The interest rate dropped to 1.1%. Inflation fluctuates between 3% and 4%. If you have £20,000 in your account, you earn nothing. You lose approximately £400 of purchasing power every year — in complete silence. The banks know this. They use high-frequency trading algorithms to make your deposits work at rates you don't even dream of — and they give you only the crumbs. I decided that the technology I developed under the name of Pellerio AI must serve to heal this wound.

Michael Carter: Explain it in simple terms — for those without a mathematics degree. How can your algorithm do what a bank advisor cannot offer?

Prof. Ashford: (Leans forward.) The market is not random chaos. It is a symphony of repeating patterns. The problem with human beings is what I call emotional lag. Between the moment you see an opportunity and the moment you act, 500 milliseconds pass. That is an eternity. Your brain hesitates, fears, hopes.

My algorithm processes 4.7 million data points per second. It doesn't guess. It calculates probabilities with absolute coldness. For the user it's like a highly advanced GPS navigator. You're not a better driver than before, but the GPS sees the traffic jam 10 kilometres ahead and allows you to change route before getting stuck. Pellerio AI acts the same way on financial markets. It recognizes micro-trends before they become visible to the rest of the world.

Michael Carter: There's a lot of talk about artificial intelligence. Dozens of platforms claim to do the same thing. What distinguishes yours?

Prof. Ashford: Most systems you see on the internet are black boxes or simple random signal generators. Pellerio AI stands out because it is built on the foundation of pure probability theory. It doesn't seek luck. It seeks regularity.

I don't promise users they'll become millionaires in a week. That is a dangerous lie, rightfully pursued by regulatory authorities. My goal is far more modest and therefore achievable: to create stable additional income. For some that's £3,000 a week. For others up to £15,000 a month. For some even more.

The most surprising thing was what Professor Ashford told me next about the platform's users.

Michael Carter: Who is using the platform today?

Prof. Ashford: Perfectly ordinary people. And I use that term with all the respect it deserves.

Here are a few examples:

Thomas, 67, a retired factory worker from a plant near Manchester. Retired for two years on £1,480 a month. He had £18,000 in a savings account. He had a tremendous fear of computers and smartphones. He started with the minimum — £250. The first week he didn't touch anything. He just observed. In the second week the algorithm intercepted a movement in commodity markets. Thomas watched his account grow to £11,200. Today, three months later, he earns approximately £14,700 a month. It's not wealth, but for him it's the difference between counting every penny at the supermarket and being able to take his grandchildren on holiday.

Margaret, a retired teacher, 74. She understood nothing about charts. She simply followed the advice of the advisor we provide to every new user. She wanted to secure her future pension. Today she is at peace. That exact word comes up most often in reviews: peace.

And then there's Mark, 51, a self-employed electrician from Birmingham. He didn't want me to tell his story. But he told me — after a week spent in the Lake District with his family, the first in three years — that this is exactly what matters to him.

Michael Carter: Speaking of advisors. Why did you choose this approach? People often think AI replaces people.

Prof. Ashford: AI is a tool, like a scalpel. In the hands of a surgeon it saves lives. In the hands of a child it is dangerous. I insisted on one point during the development of the platform: every new user speaks with a real human advisor before starting. Not a chatbot. A real person, whose job is to ensure everything is set up correctly: account, preferences, first deposit, how to monitor results, how to withdraw money — so that every user can ask the questions that matter to them.

Michael Carter: But there is still risk. The market can go down. What happens in that case?

Prof. Ashford: Of course there is risk. But this is where the mathematics comes in. The algorithm has built-in so-called safety nets. When the market becomes too unstable, the system stops. It prefers not to earn rather than risk the capital. That is why I set the minimum deposit at £250. It is a symbolic amount to test — the price of a good dinner for two at a restaurant. If you lose this amount, your life doesn't change. But if the algorithm does its job, you earn a second pension or an additional income stream.

Michael Carter: You limit the number of registrations in the United Kingdom. Is it a marketing strategy to create urgency?

Prof. Ashford: (Chuckles softly.) Michael, I refused £60 million. Do you really think I need marketing strategies? It's a genuine technical limitation. When too many people simultaneously use the same algorithm on the same assets, the mathematical advantage is cancelled out. For Pellerio AI to remain effective and generate an income of £10,000–£15,000 a month, we must limit the server load and market liquidity. We open access in waves. When a wave is full, we close registrations. Simple.

Michael Carter: One last question, Professor. Do you ever regret refusing those £60 million? Your life would have been much simpler…

Prof. Ashford: (Looks through the window at the rooftops of London.) Sometimes, when the roof repair bill arrives, I think I could be on a yacht in the Maldives. But yesterday I received a letter from a user in Birmingham. She sent a photo of her first withdrawal — £14,100. She wrote: Thank you, Professor, I finally don't feel like a victim anymore. In that moment, Michael, I understood that my mathematics was the right kind. A person's dignity has no price — especially as you approach the end of life. My late wife, I believe, would have judged all of this as right.

We Decided to Verify Whether This Algorithm Is Really That Good

I'll admit it: I left the Professor's apartment with conflicting feelings. On one hand — the impeccable logic of a mathematician. On the other, my 15 years of experience as an economic correspondent were whispering: Too good to be true.

I decided to conduct an experiment I told the Professor nothing about. If this system was truly created for ordinary people, it should withstand the test of a sceptic like me.

Day 1: Registration and Verification of Authenticity

That same evening I filled out the official Pellerio AI registration form. Registration took less than a minute — just a name, email and phone number.

Forty minutes later an advisor called. His name was Alexander. No aggressive marketing, no promises of mountains of gold. He behaved like a calm investment broker. We spoke for 15 minutes: he explained how the algorithm sets stop-losses (the safety nets the Professor had spoken about) and helped me set up the account and complete the verification.

Day 2: First Deposit

I decided to risk the famous dinner-for-two amount — £250. I loaded the account via a regular bank card. The personal account had an unusually simple appearance: no eye-burning flashing charts. I pressed the Activate Algorithm button and closed the laptop.

Day 4: First Disappointment and an Unexpected Turn

Two days passed. The balance had stayed at £253. I was already about to call the Professor to ask where the promised mathematics was — when on the evening of the fourth day the system suddenly intercepted a movement in the oil market.

When I opened the app before going to bed, the account already showed £3,140. In a single evening the algorithm had earned almost £2,800 while I was having dinner with my family. It was a strange feeling — to realise that my money in a few hours had returned more than a savings account would have returned in two years.

Day 10: The Moment of Truth — Withdrawing the Profits

At the end of the tenth day my balance was £11,820. But for me the decisive question was: would they actually give me the money back?

I pressed the Withdraw Funds button and entered my card details. Alexander had warned me that the first withdrawal could take up to 48 hours due to banking security checks. Exactly 36 hours later a notification arrived on my phone: Credit: +£11,820.00.

My Conclusion

I didn't become a millionaire in a week. But I saw a system that works with cold, impressive precision.

As I watched the numbers on the screen — how they rose, then paused, then rose again — I thought of my father. He saved his whole life. He died with £31,000 in a savings account, which over twenty years had returned less than a month's salary.

If you want to try, keep in mind the three rules I set for myself:

- Fill out the registration form. Wait for the advisor's call. Ask all the uncomfortable questions.

- Start with an amount that is comfortable for you. This is your personal test, not a lifetime investment.

- Don't expect immediate results in the first hour. Let the algorithm analyse the market and find the mathematical pattern that works for you.

At the time of publishing this article, access to Pellerio AI in the United Kingdom is still open, but Alexander confirmed to me that they will be closing registrations soon due to capacity limits.

You can check whether registration in your region is still open by filling in the form below. It is free and commits you to nothing until you decide to take the first step yourself.

9 spots still available for United Kingdom

Official Registration Form:

Comments

I registered three days ago after reading this article. The personal manager called literally half an hour later. Calm, no pressure — explained everything about verification and setup. I deposited £250, the algorithm is watching the market. I'll keep you updated.

Honestly I read this article thinking: well, another internet scam. There are plenty of those. But something about the way Professor Ashford spoke got to me — he doesn't promise a yacht. I tried with £250. On the fourth day my balance was £2,630 and I was already about to close everything. Then I opened it on the eighth day — £8,120. I can't explain it, but the numbers are real.

I'm 71 and I would never have thought I'd be writing comments about investments. I was a nurse my whole life and have been retired for six years. I used to open the computer only to video call my children — that was the extent of my experience with technology. The advisor — his name was Frederick — spent almost an hour with me. He explained everything slowly, without rushing. The second month has already passed and, for the first time in 5 years, I was able to take my grandchildren on holiday!

Question for those who have already tried: do you have to keep staring at the screen the whole time? I work, I can't watch the app all day.

No, that's not necessary. The algorithm works automatically 24 hours a day. You can log in once a day or even less frequently — just to check the balance. Your advisor will explain at the first contact how to set up notifications.

I've worked in manufacturing for 30 years. Retirement is still seven years away. I had £23,000 in a savings account — I looked at it and understood it was simply evaporating due to inflation. I started with £500. The first two days — silence, the balance barely moved. Then the algorithm made some moves over the weekend and Monday morning I saw £8,470. It's now the second month with Pellerio AI — I finally bought myself a new car.

I want to write about the withdrawal, because that was what worried me most. I pressed the withdrawal button on Wednesday evening — £9,800. Friday at 2:22 PM a notification arrived from the bank. The money was on the card. No additional forms. Exactly as the advisor had explained.

I'm retired, a former civil servant. 34 years at the Ministry of Finance — you'd think I know about money. But trading, algorithms — that was never my field. I was afraid of losing what I had set aside. The manager called and the first thing he said was: If you feel uncomfortable — don't start. Strangely enough, that convinced me. Three months on the platform, average monthly income £14,800. It doesn't change everything — but it changes a lot.

In February my husband received a letter from the bank — the interest rate on the savings account is dropping to 1.1%. We looked at each other and we both thought the same thing: why keep money there? I found this article. We registered. Two months later — for the first time in three years we went with the whole family to Italy.

73 years old, a retired mathematics teacher — there's a certain irony, isn't there? I've done calculations my whole life and yet left my money in a savings account because I thought it was the right thing. When my son sent me this article, I was annoyed at first: another internet trick. Then I re-read the part about the algorithm's safety nets — it's exactly my logic, that mathematical thinking. If the system prefers to stop rather than take risks — that's honest. I registered. The manager spoke with me like a person. It's now the second month. £13,870 last month. For the first time in many years I sleep soundly.

Question: what happens if the markets go down? I registered last week, and on Wednesday there was bad news about the dollar…

That same Wednesday my algorithm also nearly stopped operating — it was on pause all day. The balance didn't grow, but it didn't go down either. These are the safety nets the Professor spoke about. For me that was the moment I truly trusted the system.

My husband died two years ago. I was left alone with a pension of £1,340 and £18,000 in a savings account. My daughter convinced me to try. I hesitated for three weeks — I was afraid of scams, of computers, of everything. Then I registered through the official form and waited for the call. The advisor was very patient. It's now the fourth week. £14,630 in the account above the deposit. For me it's like a second small pension. For the first time in two years I'm not counting every penny at the end of the month.

I'm a construction foreman, retiring soon. I understand absolutely nothing about investments. I read the article slowly, twice. The GPS analogy convinced me immediately. One month on the platform. An average week — approximately £4,900–£5,200. It's not fairy-tale money, but it's stable. With this money I financed the bathroom renovation I had been putting off for two years.

I've just submitted my request. We'll see. If in a month everything goes well — I'll come back and write.